States that have surpluses in tax revenue set them aside as rainy day funds for emergencies and future budget shortfalls.

Pew Charitable Trusts reports, May 17, 2021, that in the fiscal year that ended for most states in June 2020, in spite of the coronavirus lockdown and the start of a recession, many states’ rainy day funds were unchanged or even grew somewhat. Overall, rainy day funds nationwide totaled $71.6 billion—second only to the pre-pandemic record-setting total of $78.7 billion.

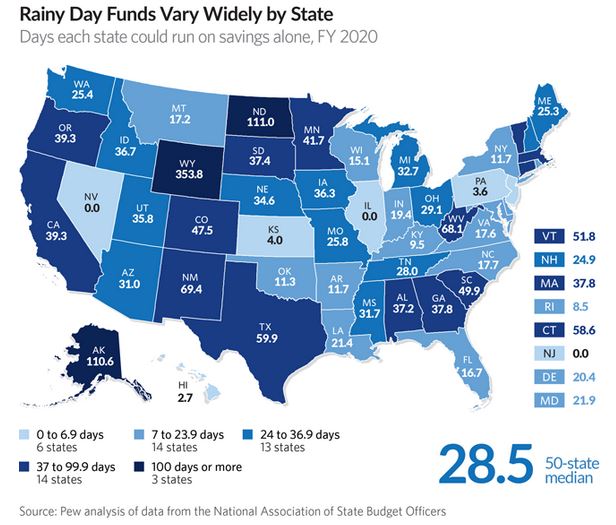

But there is a wide variation in how far each state’s rainy day funds could stretch—from enough to run government operations for almost a year in Wyoming to zero savings in Illinois, Nevada, and New Jersey. The median amount at the start of this fiscal year can cover 28.5 days’ worth of general fund spending, or 7.8%, meaning at least half of states have that much or more saved, while half have less.

Citing CNBC, GoBankingRates reports that 29 states are flush with extra cash, some of which plan to use the surplus on tax cuts or provide financial relief to residents. Those states include the following:

- New York, New Mexico and Maryland are offering payments or tax credits to low-income families.

- California has a surplus of $75 billion. Gov. Gavin Newsom, who is facing a recall election, has proposed sending $600 checks to residents earning up to $75,000 a year. California households struggling financially might also get relief on past-due rent, utility bills and traffic tickets.

- Idaho, with a $500 million surplus, is providing a tax rebate to residents who filed a 2019 tax return, in amounts of either $50 per person or 9% of taxes owed, whichever is greater. The state has also authorized a lower top tax rate.

- Other states with surpluses that have either enacted or proposed tax cuts include Montana, Oklahoma and Iowa.

~E